EXPLAINER: The making of Africa's sovereign debt crisis - Part Two

The courtyard of the incomplete trainee's hostel at the Bagabaga College of Education located in Ghana's northern city of Tamale is overgrown with weeds and looks abandoned. It has remained an unfinished construction project for more than a decade, according to Graphic Online in Ghana.

Founded in 1944, the college has trained teachers for almost 80 years and the hostel was intended to accommodate some 400 trainees – but due to funding shortfalls it has never been completed.

This hostel is emblematic of the state of teacher training colleges in Ghana. At Akrokerri College of Education, work on a new 300-bed hostel ground to a halt years ago, while the lack of maintenance at other facilities has rendered them unusable.

And all this comes at a time when enrollment at such colleges are at an all time high, so high in fact that many have resorted to a double-shift system to cope with demand.

The situation has become so chronic that teachers at a summit last year called on the Ghana Tertiary Education Commission to undertake an audit of the infrastructure at the colleges to identify and log deficiencies.

The inadequate infrastructure, which has created a bottleneck in the supply of teachers for Ghana’s primary and secondary school system, is not surprising when one views the displacement of spending on education by the rising costs to service sovereign debt. We’ll return to this issue later but first: How did it get to this?

The incomplete 400 bed hostel at the Bagabaga College of Education (Photo: Uncredited)

A quick refresher

In our first article covering the sovereign debt crisis that is sending shock waves through Africa’s politics and overwhelming the provision of public services, we described how countries used different types of debt over the course of the last decade.

We also noted how many states, even before the onset of the pandemic, were approaching the critical threshold in the measurement of government debt relative to the size of their economies, using the so-called debt-to-GDP ratio.

The World Bank thinks that above the level of 64% debt becomes unsustainable, meaning there is a much bigger risk of the country becoming financially distressed – as in not being able to meet payments as they come due.

We also showed how much borrowing by African governments was being done in foreign currency - typically the U.S. Dollar, but sometimes in Euros or Yuan. This external debt increases the risk to the borrower because exchange rates can swing massively over the course of a loan.

And remember, all this was happening in the years before the lockdowns of the Covid-19 pandemic in early 2020.

So then what?

Beginning in March 2020, countries, regions and eventually the entire world entered “lockdown". This was unprecedented in modern history, forcing people to stay at home and bringing entire economies to a standstill.

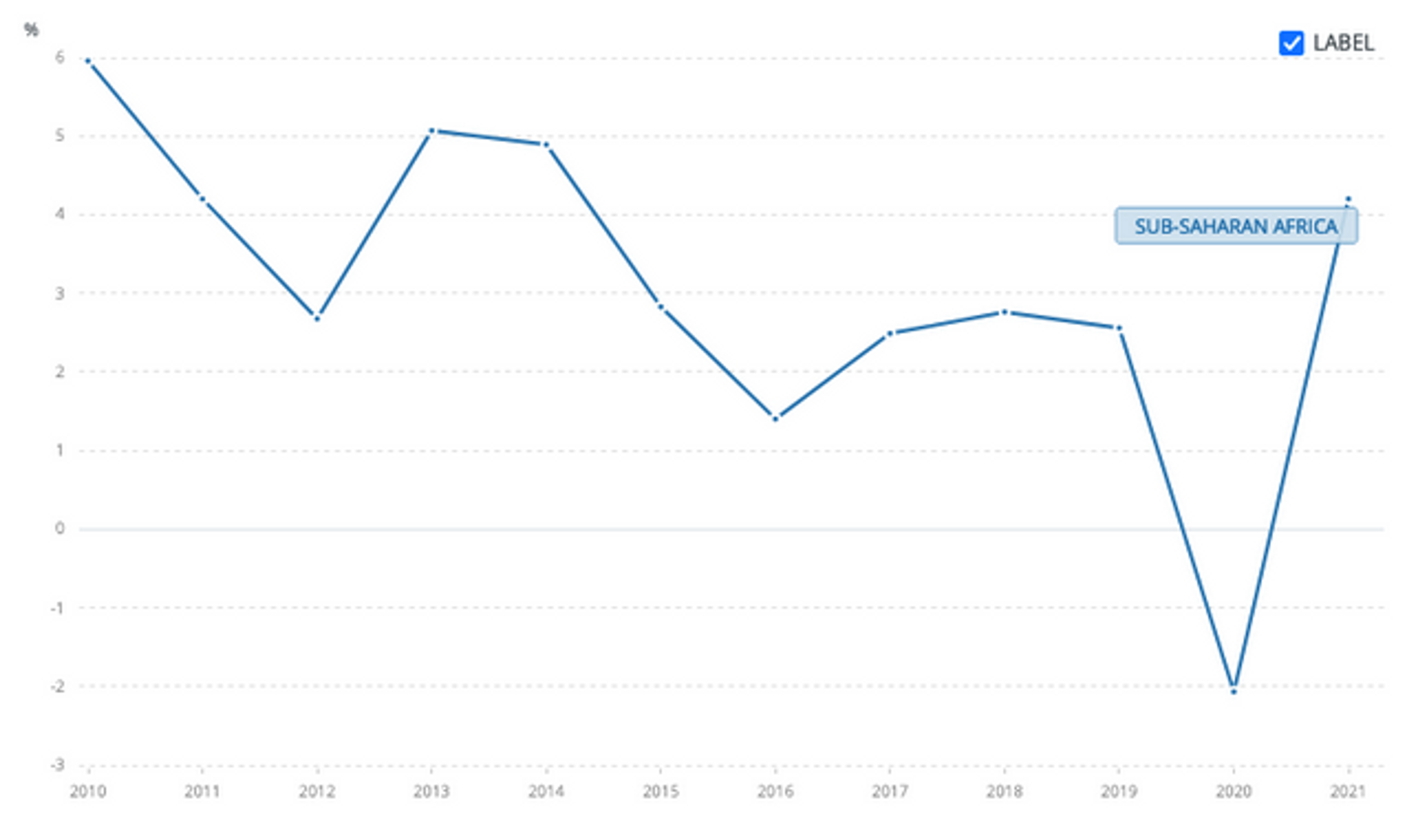

From an economic perspective, Covid-19 was an unmitigated disaster. The graph below shows Sub-Saharan Africa’s (SSA) GDP from 2010 - 2021 and you can see the onset of Covid. Simultaneously, while economies shut down, government finances were under enormous pressure to provide resources to enable public health systems to cope with the disease. This also led to more borrowing.

Sub-Saharan African GDP growth rate, 2010 - 2021 (percentage)

(Source: World Bank)

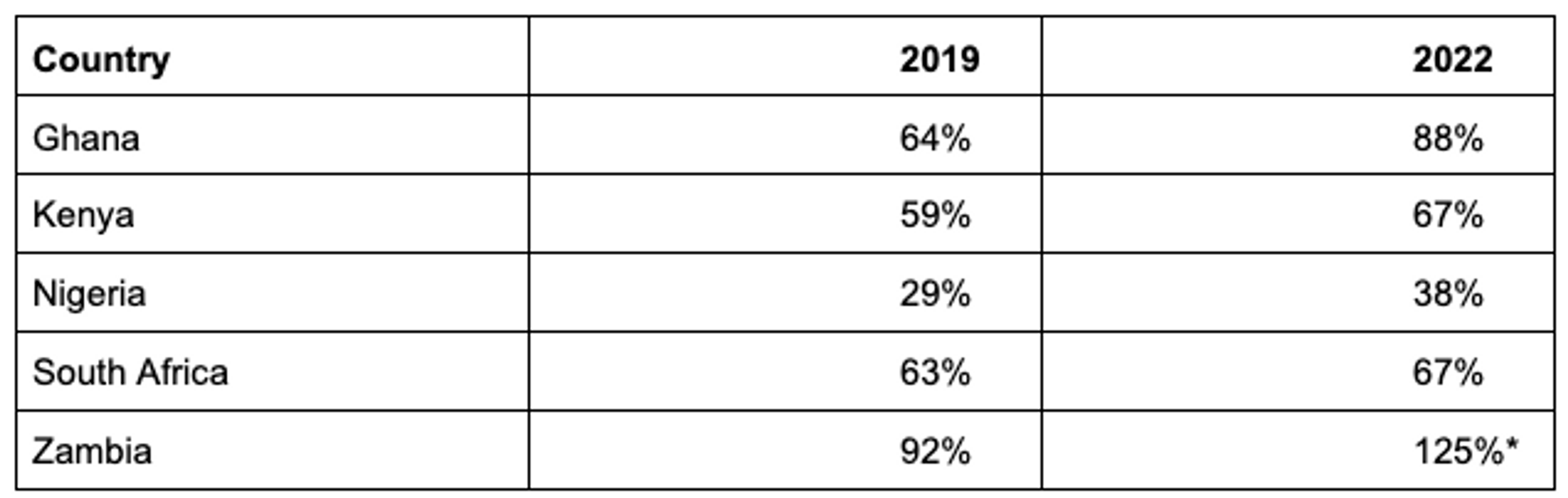

So presumably African countries became more indebted?

They did, even despite the strong economic recovery that occurred in 2021 (see above graph). Using the same sample from our first article, you can see how things developed (below).

Government debt as a percentage of GDP for select African countries, 2019 vs. 2022

(Source: Trading Economics. *estimated.)

Remember that crucial threshold the World Bank warned us about? The 64% line above which managing debt becomes tricky. Well, most of the countries in the table are above that. Covid is when things start turning nasty.

Should I cover my eyes?

It’s not pretty. Covid-19 changed things in ways we didn’t understand at the time. In the Western world, governments threw so much money at the problem on the concern the pandemic could trigger a lengthy global recession.

The Americans, for instance, spent the equivalent of 20% of GDP across various programmes run by the Federal Government to counter the medical and economic effects of the pandemic. Many other countries acted similarly.

The net effect was actually a good news story: the global economy recovered quickly. But the timing and extent of reopening economies varied widely across countries – which grotesquely disrupted global supply chains. China, for instance, with its strict zero-Covid policy, kept its vast manufacturing base closed for longer than other parts of the world. And just as we were putting Covid behind us, Russia invaded Ukraine.

And so?

Costs started to rise because as people’s jobs and incomes recovered, demand for goods and services increased rapidly. However, the complex global logistics and supply chains that fed them were in disarray.

This, according to economists like Joseph Stiglitz, together with the effect of the war on the price of energy and agricultural commodities, led to dreaded inflation!

What does inflation have to do with the sovereign debt crisis?

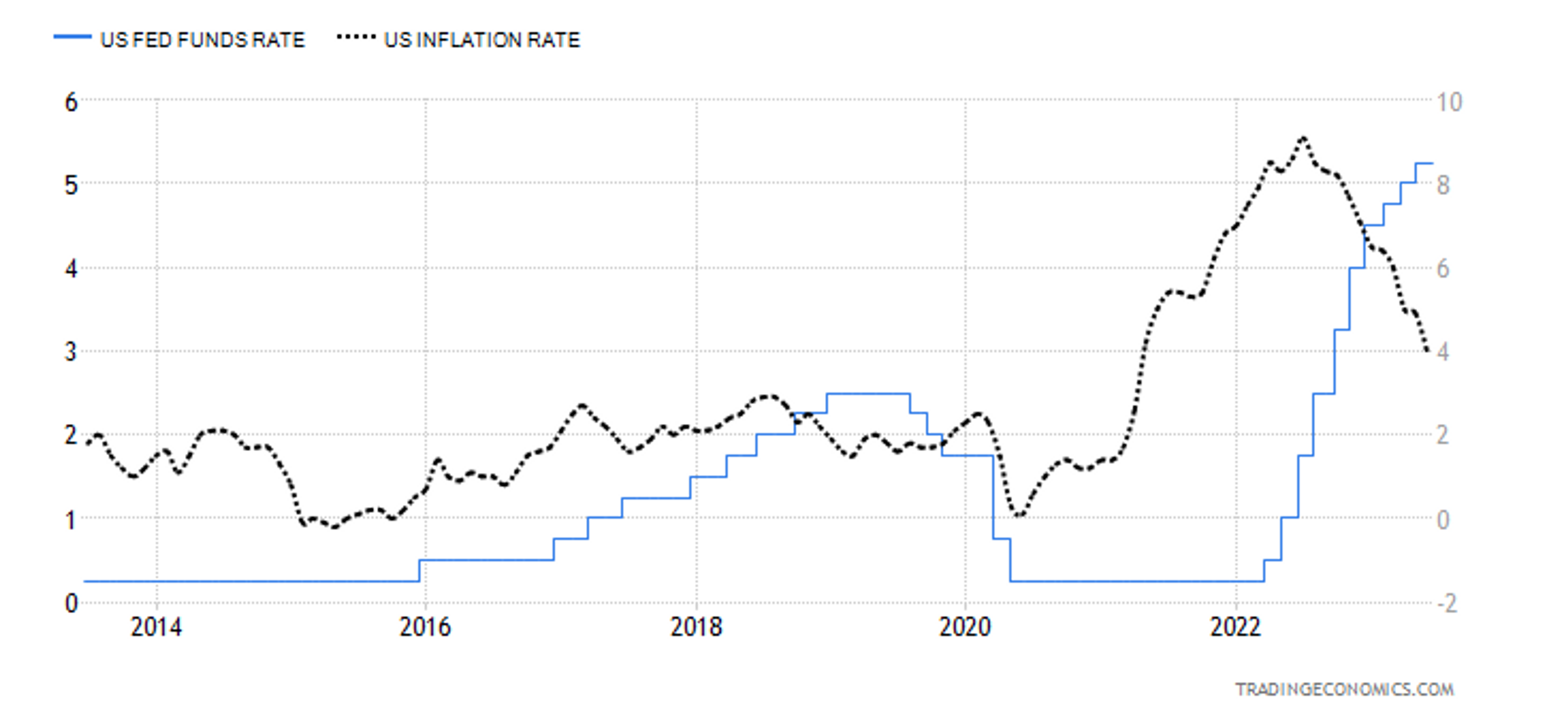

If Covid-19 was the tick in Africa’s debt bomb, then the tock was inflation. Because the problem with inflation is that if it sticks around, at some point monetary authorities have to raise interest rates to choke off demand. It’s a blunt weapon, but one of the few tools that central banks have.

A look at the graph below shows U.S. inflation rates (black dotted line) peaking at 9% at the start of last year just after the U.S. central bank began raising interest rates (blue). U.S. interest rates have gone from virtually zero to five percent inside of eighteen months.

U.S. Inflation and central bank (Fed Funds) interest rates, 2013 - 2023

(Source: Trading Economics. Blue line: Fed funds rate - left axis. Black line: U.S. inflation - right axis)

Africa’s external debt stood at $645 billion at the end of 2021 according to data collated by ONE. So when interest rates start rising as quickly in the United States as they have over the last 18 months, there are usually other consequences…

Goodness, does this ever end?

So it was a bit of a case of ‘everything that can go wrong, will go wrong’ because much of the money invested in developing economies in the last decade was due to interest rates (or what investors refer to as ‘yield’) being so low in the Western world.

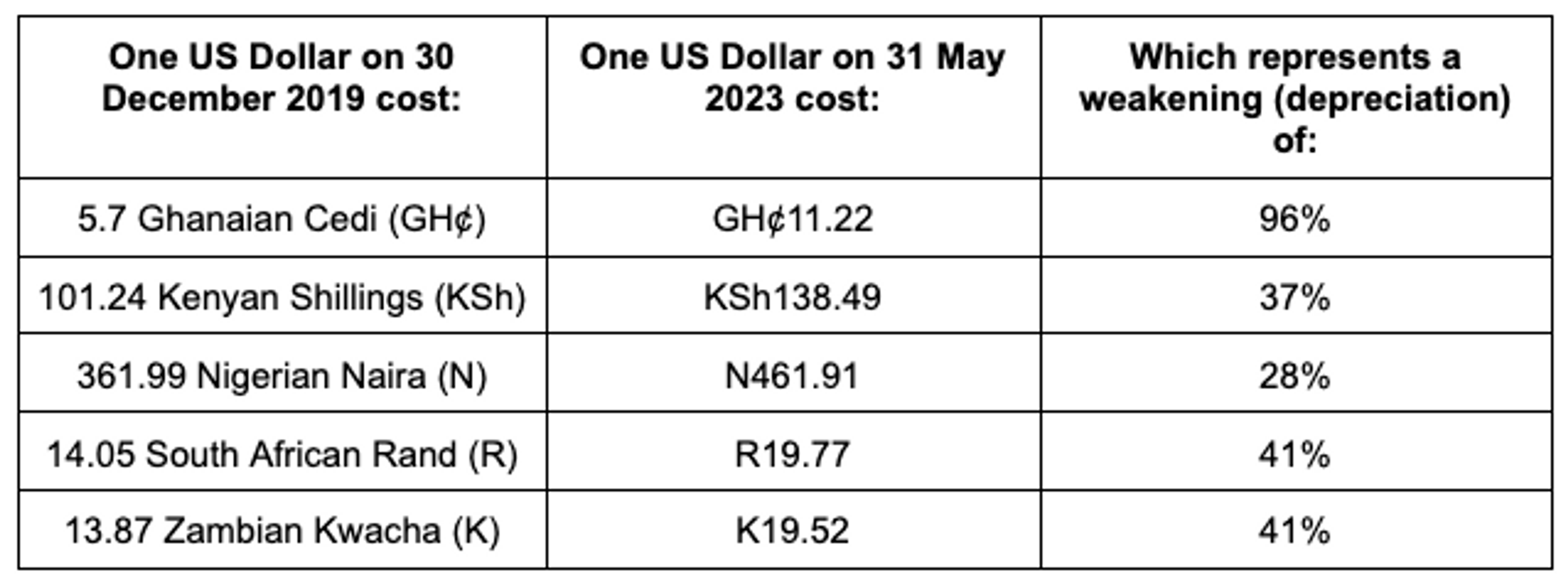

The sharp rise in interest rates rapidly changed the equation and much of this money began returning “home”. And while there are other dynamics in play in foreign exchange rates, this was significant and has contributed to the weakness (depreciation) of African currencies as seen below:

(Source: XE.com. Author's calculations)

Besides paying more for U.S. dollar denominated loans as a result of rising interest rates, the debt in local terms has increased substantially as a result of currency depreciation. Ghana’s foreign-denominated debt (using the table above) is now double what it was prior to the pandemic, just on account of the 96% depreciation in the Cedi over that time.

Detonation!?

Yip, kabluey.

Basically: pre-pandemic indebtedness + rising interest rates + currency depreciation = full blown sovereign debt crisis.

And it’s not just Africa either.

But beyond using government debt-to-GDP, an even more useful indicator to establish the effect sovereign debt is having on individual countries is to look at debt services costs as a percentage of government expenditure.

Debt service costs include interest and capital repayments. In the case of bonds, when the bonds mature, the borrower has to pay the full amount back. Very few countries usually have the cash on hand at the time to repay the capital, and consequently have to reissue another bond or take out a loan in which to pay investors back. Africa's debt repayment bill on its external debt will reach $68.8bn this year, and is estimated to peak at $74bn next year (2024) before it eventually begins to decrease.

The effects of all this on vital services for the ordinary populations is significant

As governments struggle to find even more money to pay the interest on their loans, that cash has to come from somewhere. And you guessed it, the bean counters in government finance departments across the continent see the budgets for social spending on education, health and welfare evaporate. The debt service bill obliterates everything.

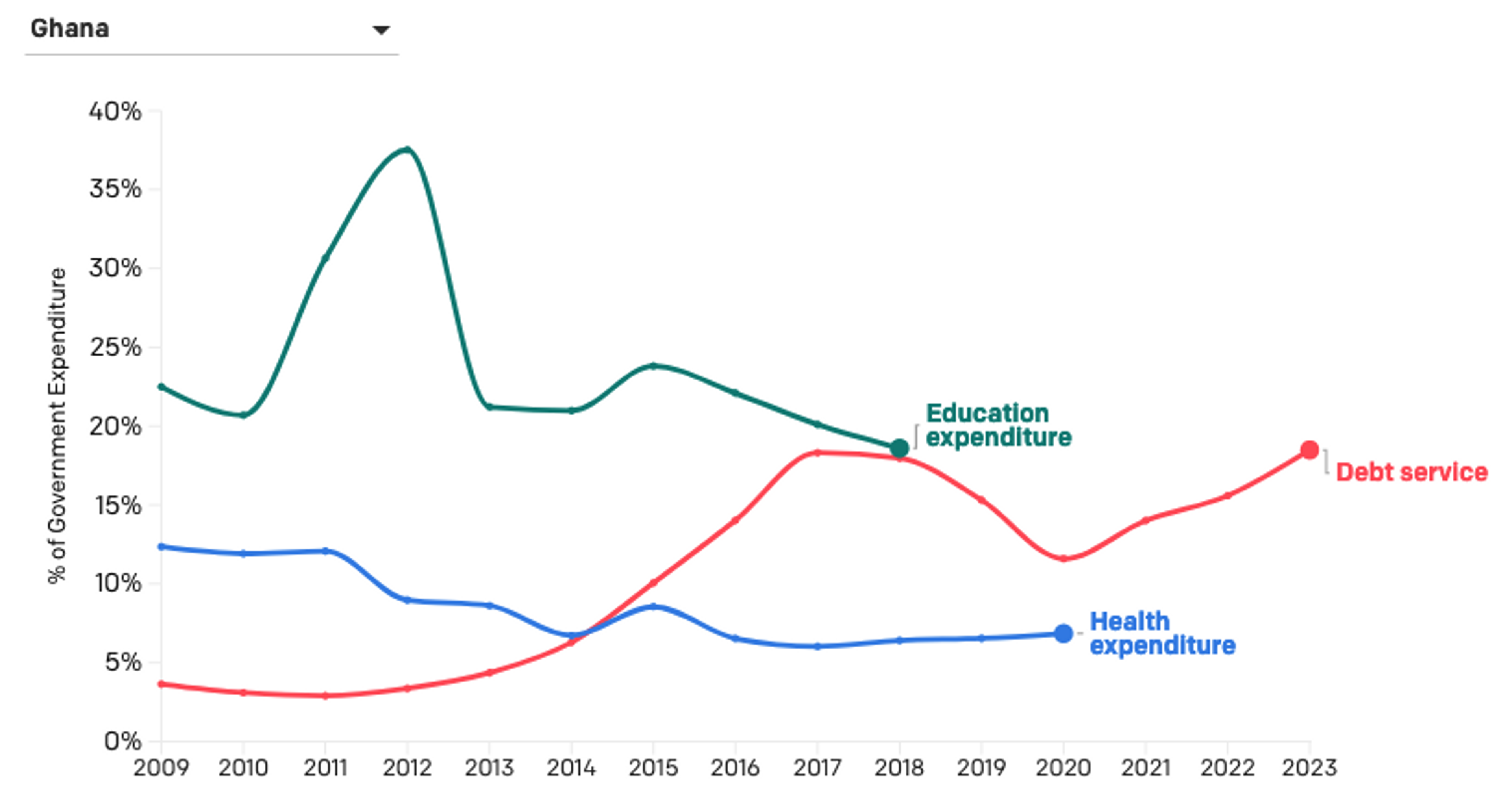

The graph (below) compiled by the anti-poverty campaign group, ONE demonstrates how Ghana's debt service costs rose in relation to the decline in government health and education spending. You can view the interactive map here.

(Data collated by ONE)

Got it!

Good. With this economic context in mind, let’s return to Ghana’s teacher training colleges. Like many African countries, Ghana’s population is extremely youthful, and together with government moves to introduce free senior high school, enrolments at tertiary institutions have increased every year since 2006.

There are now over half a million students enrolling every year for some form of tertiary education . This is a really positive development. Many of these tertiary students want to become teachers.

In 2013, when many of the hostels were being built or contemplated, the nation’s external debt stood at $11.24bn. It is now $27bn.

The rise has seen a painful squeeze on government resources - the budget for education as a percentage of government expenditure has been falling more or less every year since 2012, eaten up by Ghana’s rising debt service costs. So gaps were bound to appear, and many of them have been found at the teachers training college, between the roof and the floor, where the walls have yet to be completed.

But many of the consequences are less tangible - teachers not trained, students not taught, lives not enriched. The direct impact on the quality of people’s lives should always be top of mind when we consider the sometimes bland subject of sovereign debt.

* Be sure to look out for more as we explore the topic in depth over the coming months. Please email me at [email protected] if you'd like to help me investigate this subject with tips, suggestions, contacts and advice. Thank you.

* More about Warren Thompson here.

* Artwork: Clement Kumalija