Low tax guaranteed: how a Russian mining giant has saved $16.5m in Burkina Faso – one of the world’s poorest countries

The impoverished citizens of Burkina Faso have missed out on an estimated $16.5m in gold mining royalties that could have funded vital public services thanks to a special low tax deal its former dictator made with a foreign firm.

The sum easily eclipses the $12m the West African country allocated for school supplies across the entire nation this year.

The owner of the mine currently reaping the benefit of the tax deal is Nordgold, which is itself owned by one of Russia’s richest men – Alexei Mordashov (right), who has an estimated $19bn fortune.

Described by the World Bank as a least developed country, life expectancy among Burkina Faso’s 19 million population is 60 years. Its literacy rate is just 36%.

Golden years

Today, Burkina Faso is Africa’s fourth biggest gold producer, with the precious metal now accounting for 75% of its total exports.

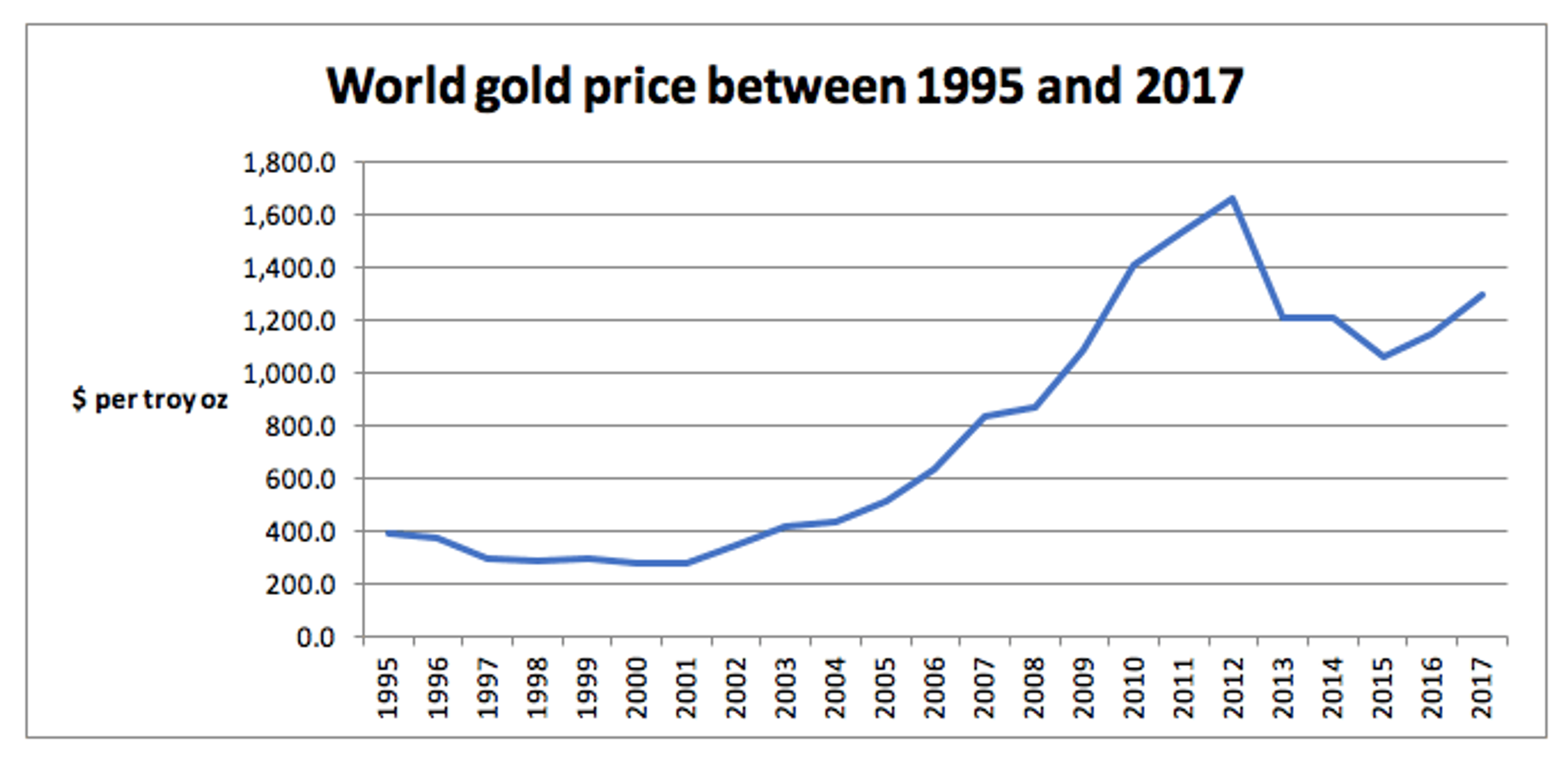

The boom has largely happened since 2002, the year in which gold prices began to rocket. Burkina Faso’s royalty rate of 3% – a tax on sales revenues – was considered low and overseas extractive industry companies rushed to what was regarded as an investor-friendly country.

Companies made healthy profits but there was growing concern the government was not benefitting enough from the commodity.

Disquiet in 2010 prompted the then-government of Blaise Compaore (left), a brutal dictator, to increase royalty rates on gold.

Compaore’s government introduced a new floating royalty mechanism in line with the world gold price.

It meant that when the world gold price was less than $1,000 per ounce, the existing 3% royalty would be maintained.

But if prices went above $1,000 per ounce, the rate would rise to 4%.

Above $1,300, companies would pay a 5% royalty levy.

At the time of the new arrangement, the world gold price was more than $1,400 per ounce.

But, exceptionally, at Nordgold’s Taparko mine, these new rates did not apply due to a highly controversial agreement made 15 years earlier with the mine’s previous owner.

Disclosures & data

A joint investigation between Finance Uncovered, L’Economiste of Burkina Faso and Cenozo, the West Africa investigative journalism unit, focused on the Taparko mine in Namentenga province, about 200 km northeast of Ouagadougou, the country’s capital.

Taparko is the fifth biggest mine in Burkina Faso. Since 2011, it has produced gold worth over $1bn.

We have obtained a copy of a contract which shows that in 1995, the previous owner of Taparko, Canada’s High River Gold, successfully negotiated a deal with Campaore’s regime to fix the royalty rate at 3% for 25 years.

This low tax guarantee is known as a fiscal stability clause.

And these deals, which were introduced to attract foreign companies worried about uncertain fiscal and political environments, have become highly controversial in policy circles because they override any future changes to a country’s legislation.

Incredibly, it seems the Burkina Faso government had even forgotten about the clause in 2011 – by which time the mine had been bought by Nordgold.

According to Halidou Bocoum, director of Nordgold in Burkina Faso, that year the government attempted to charge the Taparko for royalties at the new higher royalty rate.

Nordgold’s bosses wrote to the government to complain and Bocoum said they received confirmation of the “continuity of the tax regime”.

Our investigation confirmed this was the case. We looked at Nordgold’s own disclosures in its annual reports and established it has been charged a royalty rate of just 3% every year since the new rates were introduced – despite the gold price being well above $1,000 per ounce throughout.

Using Burkina Faso Ministry of Mines gold production data, we calculated Nordgold made a $16.5m saving thanks to this low tax guarantee.

But a Nordgold spokesman said it had contributed massively to the country’s economy. He said: “Since 2009, Nordgold has paid more than $320 million to the Government of Burkina Faso in the form of taxes and royalties, and in 2016 alone this figure was around $55 million, or about 17% of Burkina Faso’s revenues from the mining sector.

“Far from ‘escaping’ taxes … Nordgold has been a proud and significant contributor to the growth of Burkina Faso’s economy.”

But Kwesi Obeng, Oxfam International’s West Africa regional programme advisor, said our investigation again highlighted the problems with fiscal stability clauses.

He said: “In Africa, as in this case of Burkina Faso, most fiscal stability clauses are asymmetrical, protecting the mining company from adverse changes (and are) beneficial to the individual investor. This undermines the state’s ability to mobilise its fair share of revenues to finance sustainable development.”

Campaore was ousted in a military coup in 2011 and fled the country but if Burkina Faso’s new regime wanted to remove this guarantee, it could attempt to negotiate with Nordgold again.

If Nordgold refuses, Burkina Faso could impose a tax or annul the contract. This, however, would risk Nordgold taking Burkina Faso to an international arbitration court which can be very costly and time consuming.

But the stakes are high. Nordgold is expected to produce even more gold from Taparko and potentially benefit from even greater royalty savings. This is because Nordgold recently confirmed that it is “studying an underground mining option in Taparko that could significantly extend the life of the mine”.

Taparko, however, is not the only mine Nordgold owns in Burkina Faso. Nordgold’s biggest gold operations are at Bissa and Bouly which last year generated sales of $402m – triple the $136m revenues produced at Taparko in 2017. These mines do not benefit from stability clauses.

What are Fiscal Stability Clauses?

When governments allow oil, gas and mining companies to extract valuable resources, the rates of tax and royalties are probably the most crucial part of the negotiation.

Royalties are levied on the revenue generated by a mine whereas taxes are imposed on overall profits.

Government often try to impose higher taxes so countries benefit from valuable natural resources.

Companies, however, want low tax and royalty rates so they can make more profits from their investment. Companies also like certainty over the taxation system. They prefer assurances that the taxation regime will not change. This makes it easier to predict cashflow.

To protect themselves, companies often request legal guarantees that state if governments increase taxes on extractive industry projects, their specific mines are not affected by higher taxes.

These are known as fiscal stabilisation clauses. They are controversial because they can override national laws. Most extractive contracts do not contain fiscal stabilisation clauses because countries can lose a lot of money that way.

Over the past ten years the gold price has risen sharply. So companies that inherit a fixed royalty rate built into their contract, like Nordgold, can save themselves a lot of money.

Executive director of Tax Justice Network Africa, Alvin Mosioma sees what has happened at Taparko as part of a wider problem: “Stabilisation clauses have in, recent times, become a bone of contention between governments and multinationals operating in the extractives sector,” he said.

“As economies come under more pressure to generate revenues internally, and in effect improve policy around foreign investment, they are forced to look more critically at investment agreements signed between themselves and multinational companies.”

Mosioma concludes: “In the end, state’s ability to align its fiscal policy to changing domestic economic priorities and support domestic resource mobilization is severely limited owing to the protectionist nature of stabilisation clauses.”

Written by J.B., Daniela Quirós-Lépiz and Nick Mathiason Edited by Ted Jeory This story is also published in L’economiste du Faso and by Cenozo Main image: Taparko gold mine from Nordgold website.