From debt to death on the streets: Just how big is Africa's loans crisis?

How damaging is the sovereign debt crisis gripping Africa? Is it a significant problem for the continent?

Well this whistle stop tour of some of the continent’s largest economies aims to explain the quantum of the challenge and perhaps reinforce the principle that individual countries can learn from one another.

Egypt

Let’s move from Cairo to the Cape and begin our trip in Egypt where president Abdel Fattah el-Sisi who, as the incoming president of NEPAD (The New Partnership for Africa’s Development), has committed to intensifying efforts to find solutions to the continent’s accumulated debt crisis.

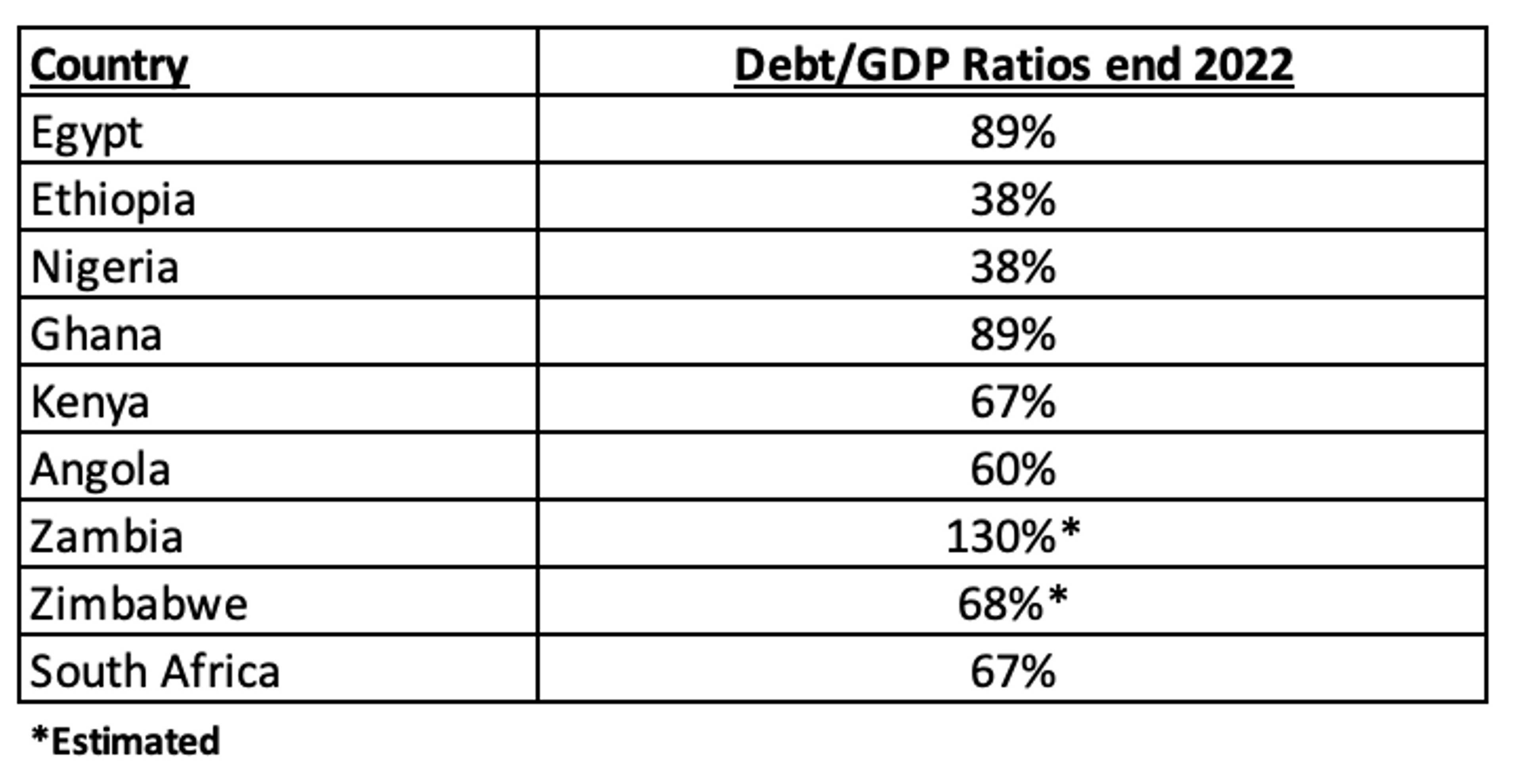

The World Bank considers debt-to-GDP ratios above 64% for developing countries as unsustainable. But in Egypt, debt-to-GDP reached 88.5% last year. It is projected to rise even further in 2023.

A $3bn loan agreed with the International Monetary Fund (IMF) in December should persuade other funders to provide the estimated $20bn Egypt needs this year to see it through its tough patch.

Most of the money ($13bn) will be used towards plugging the difference between imports and exports as it scrambles to find enough hard currency to pay for things like wheat imports. Compounding the situation is that the Egyptian pound has lost roughly half its value against the U.S. dollar over the last two years.

In return for its $3bn bail out, the government promised the IMF to move the Egyptian Pound towards a flexible exchange rate regime, reduce inflation, cut spending in relation to tax revenues and reduce state control of the economy by selling or closing state-owned entities (SOE’s). But reforming SOE’s is notoriously difficult.

Ethiopia

We have time to reflect on the role of state-owned entities as we head from Cairo to Addis Ababa to catch our flight aboard Ethiopian Airlines.

If you have travelled anywhere on the continent recently, it probably included a flight on Ethiopian airlines which provides a beacon for how other SOE’s across the continent should be run. The airline is on track to generate $6.1bn in revenue this year and contribute nearly $1bn in profits for its 100% shareholder, the Ethiopian government.

Ethiopia’s public finances appear to be just as prudently managed with one of the lowest debt-to-GDP ratios on the continent at 38%. While the country is borrowing from the IMF, this is not to get out of trouble. Rather, it is to support Ethiopia’s homegrown economic reform agenda that aims to stimulate the industrialisation of the local economy and will include launching a stock exchange.

Data sources: Trading Economics and IMF

Nigeria

It’s aboard flight ET 921 to Accra that we catch a glimpse of the Nigerian delta that straddles nine states on the southern tip of the country and which is home to over 32 million people. The Delta has been a blessing and a curse with its abundance of oil reserves estimated to be in the region of 32 billion barrels. At current production, it generates revenue of approximately $37bn a year.

While Nigeria has recently repaid a $500m Eurobond, analysts are worried that the country may have squandered the opportunity to significantly reduce public debt last year when oil prices were higher. The budget deficit is estimated to have risen in 2022 mainly owing to high fuel subsidies.

While its debt-to-GDP ratio at 38% looks manageable, audit firm KPMG expects Nigeria’s debt service costs will rise from 80% in 2022 to over 100% of government revenue this year, far above the 22.5% forecast by the World Bank.

Ghana

After landing in Accra, Ghana, we’re off to follow negotiations between the government led by Finance Minister Ken Ofori-Atta (pictured below) and a range of official (foreign government) and private creditors.

Ghana is attempting to plug a $15bn hole in its finances over the next few years. It reached an agreement in May with the IMF for a $3bn loan. The country hopes to secure a further $2bn from other multilateral lenders (like the World Bank) in the short-term.

The remaining $10bn in savings it needs to make will have to come from reducing the $30bn owed to foreign lenders. These uncomfortable negotiations are already underway. Ghana hopes to conclude them before the IMF returns in September.

Kenya

Back aboard our favourite airline and we’re flying east to Kenya. There is an eerie atmosphere as we drive from Jomo Kenyatta airport into downtown Nairobi. The streets are unusually quiet and there is a visible police presence in the city.

The country has been rocked in recent days by protests over the cost of living and the new finance bill. These have turned ugly as protesters clashed with police and the violence has resulted in the deaths of over 20 people. The protests called by opposition leader, Raila Odinga, intensified over the last week (17-21 July).

Kenya’s public finances are in dire straits. Over the last year, Kenya spent more money on servicing its debt than all other items in the national budget combined. The despised finance bill seeks to raise taxes in all sorts of ways at a time when consumers are already feeling the brunt of inflation.

In the last month, and probably out of sheer desperation, Kenya turned to the IMF and announced on Monday 17 July that it had secured $1bn under existing facilities to help alleviate some of the pressure.

Kenya’s problems date back to 2014 in the early days of President Uhuru Kenyatta’s administration, when the government decided to source half of its annual borrowing requirement from foreign lenders and began issuing Eurobonds.

This was fine when the Kenyan Shilling was stable, but in the aftermath of Covid, the shilling - like many other developing market currencies - depreciated. One U.S. dollar costs 31% more now than it did just two years ago, which has magnified the amount of money the government must repay on its KSh 9.6 trillion ($71.3bn) debt.

Serious questions are also being raised over how prudent and careful the government has been in managing its borrowing. A recent documentary series by Africa Uncensored (which Finance Uncovered helped produce) investigates the scandal surrounding the (non)construction of the Arror and Kimwarer dams.

In 2017, Kenya paid hundreds of millions of euros in fees and advance payments related to the projects, which have never come close to being completed. The documentary by Africa Uncensored will pursue the reasons for such a failure.

Angola

From Nairobi, it’s time to travel back to the west coast as we land in Luanda, Angola. After years of economic mismanagement and neglect under the Dos Santos family, the country became financially distressed long before Covid emerged.

In December 2018, Angola struck a deal with the IMF to borrow $3.7bn over three years.Two years later, government debt-to-GDP ratio peaked at 120%.

Angolan president Joao Lourenco (who succeeded Jose Eduardo Dos Santos in 2017) committed to an ambitious reform programme, promising to privatise 195 state assets. But many of these companies are unfit for sale and will probably have to be closed.

Lourenco moved swiftly to prosecute the Dos Santos family for corruption and recover funds believed to have been embezzled by the family. This has included targeting Isabel dos Santos, who is facing legal challenges in three countries and who has been effectively exiled in the United Arab Emirates.

With better management of its finances, the country (which is a large oil exporter) used the revenues from higher oil prices in 2022 to reduce its debt-to-GDP to 60%. This prompted an upgrade in its credit rating and allowed the country to issue a $1.75bn Eurobond last year. Angola will use some of the proceeds to repay debt that was deferred during the pandemic, and its interest costs are expected to amount to 23% of government revenues this year.

Zambia

From Angola, we head to Zambia where the country under president Hakainde Hichilema is dealing with its $28bn debt headache, most of which ($21bn) is external.

But in doing so, Zambia has found itself in the middle of a tug-of-war between superpowers competing for influence. Besides a range of western based creditors, Zambia owes money to a variety of Chinese lenders which include the Chinese government and state-owned entities. The Export Import Bank of China, for instance, is owed $4.1bn.

While creditors were being asked to take “haircuts” – financial slang for sharp write downs on the amounts they are owed, it appears China was unhappy that the IMF and World Bank were not being asked to share the pain.

There was also a feeling that China - as the largest lender to the developing world - was unhappy being dictated to, which it felt prevented it from solving Zambia’s repayment problem in other ways.

After months of negotiations, Zambia clinched a deal in June with official creditors. It appears to have secured very generous terms. By one account, it will only have to repay $750m in the next decade (as opposed to the original $6.3bn). For the first three years, Zambia is obligated to pay interest amounting to just $75m a year.

The deal also means Zambia can resume borrowing from other Multilateral Financial Institutions (MFIs). The country intends to negotiate with private creditors (who are owed $6.8bn) to try and secure further concessions that will ease its path back to financial sustainability.

With all these strained African government balance sheets, it's time to continue south. As we climb out of Kenneth Kaunda International Airport, we are confronted by the enormous mass of water encompassing Lake Kariba.

Zimbabwe

Zimbabwe’s financial predicament has been apparent for sometime. Defaulting on its obligations in the 00’s and failing to clear its arrears has disqualified the country from borrowing from MFIs which include the African Development Bank (AfDB).

Under the regime of Emerson Mnangagwa, Zimbabwe committed to a mediation process led by AfDB President, Akinwumi Adesina, and former Mozambican president Joaquim Chissano. The purpose of these engagements - referred to as “Structured Dialogues” - between the government and a team of technical experts, is to find consensus on a broad range of economic, monetary and political reforms that Zimbabwe must undertake to clear its name and normalise its relationship with the international community.

One of the key requirements is that Zimbabwe holds free and fair elections next month. But controversy over publication of the voter’s registration roll and the signing into law of a number of draconian bills, may well cast a long shadow over its chances. The threat of political violence and intimidation in the build-up to the elections looks very real.

South Africa

As we enter South African airspace, it is worth noting that while the country is not in a crisis with government debt to GDP sitting at 67%, it is not yet out of the woods. South Africa has a massive advantage over many of its peers in that it sources most of its borrowing in Rands and is largely immune from wild swings in debt repayments that come with foreign debt.

But the economy has barely grown in the last five years, as the government persists in trying to control strategic sectors of the economy through state-owned enterprises in which it appoints executives based on political allegiance and not competence. This has led to much of the rot at state-owned entities like Eskom.

And despite talk of a clean up after the dark years of State Capture, corruption and lawlessness under President Ramaphosa is arguably worse than it was under his predecessor, Jacob Zuma. Sadly, the section of the population that appears to have borne the brunt of the economic incompetence are the youth - with nearly one out of two people under the age of 30 unemployed as of March this year.

Where next?

So as we take in the magnificent sight of Table Mountain in Cape Town, we begin to appreciate the magnitude of the problem affecting citizens in all corners of the continent. Countries are at different stages of managing the crisis. There could yet be more angry public protests as governments confront hard choices about where they spend their next Naira, Shilling or Kwacha. The crisis might well see governments facing imminent elections, being voted out in favour of parties that promise less austerity.

But there also needs to be a review of foreign borrowing and the role this type of lending has played in the sovereign debt crisis. When should governments borrow in foreign currencies? What projects should be financed? What is a responsible limit? How can the process become more transparent? What changes need to be made to legislative and governance institutions in each country to enable better debt management? The answers to these questions should form the basis of preventing this crisis from happening again in the future.

For every problem there is a solution, and that is what we hope to be addressing in the coming weeks.